The ARM Discount: How America Learned to Stop Worrying and Love the Time Bomb

A $150 Monthly Savings on Your Path to Foreclosure

The real estate industrial complex has announced, with the giddy enthusiasm of a arsonist hawking discount matches, that American homebuyers can now "save" $150 per month by choosing an adjustable-rate mortgage over a fixed-rate loan. This represents, we are told with straight faces, the "biggest discount since 2022."

Let us pause to absorb the pure, uncut absurdity of this framing.

We are sixteen years past the moment when adjustable-rate mortgages metastasized into a financial plague that destroyed the global economy, evaporated $16 trillion in household wealth, and turned entire neighborhoods into dystopian galleries of foreclosure signs. The adjustable-rate mortgage — that beautiful Trojan horse of introductory rates and deferred consequences — became synonymous with predatory lending, financial illiteracy, and the kind of systemic fraud that would make a carnival barker blush.

And now? Now we're celebrating a 5.8% "discount."

The Mathematics of Amnesia

The typical homebuyer, according to recent analysis, would cut their monthly payment by approximately $150 by choosing a 7/6 ARM instead of a 30-year fixed-rate mortgage. This assumes, of course, that said buyer:

- Plans to sell or refinance before the rate adjusts (the exact assumption that immolated millions of households in 2008)

- Possesses a crystal ball regarding future interest rate movements (a technology not yet invented)

- Believes that saving $150 now is worth the risk of paying $500 more later (the financial equivalent of eating dessert first because you might not be hungry for dinner)

- Has somehow never heard of the years 2007-2010

The ARM, for those blissfully ignorant or willfully forgetful, is a mortgage where the interest rate starts low and adjusts periodically based on market conditions. It's the financial instrument equivalent of a first free hit from your dealer — an introductory offer designed to get you hooked on a payment you can afford, before the terms shift and the real cost reveals itself like a subplot twist in a horror film.

The Salesmanship of Selective Memory

What makes this particular carnival of cognitive dissonance so exquisite is the framing. Not "Risky Mortgage Product Returns to Haunt New Generation" or "Financial Industry Reintroduces Weapon of Mass Foreclosure" but rather: Homebuyers SAVE Money!

This is marketing genius of the highest order — the kind of linguistic jujitsu that would make Orwell weep into his typewriter. We've taken the signature product of the housing bubble, repackaged it as a savvy financial decision, and convinced a new generation that they're getting a deal.

The $150 monthly "savings" is real, of course. So is the $150 you "save" by buying the cheaper parachute. The question isn't whether you're spending less money now. The question is what happens when you pull the ripcord at 10,000 feet.

The Return of the Adjustable-Rate Mortgage: A Love Story

Why are ARMs back in vogue? Because fixed-rate mortgages have climbed to levels that make homeownership genuinely unaffordable for vast swaths of the American middle class. When the 30-year fixed rate hovers around 7%, and median home prices have achieved escape velocity from median incomes, desperate buyers start looking for creative solutions.

Enter the ARM: the payday loan of mortgage products, now rebranded as "strategic borrowing."

The financial services industry, with the memory span of a goldfish and the ethics of a loan shark, has decided that 2008 was just a little oopsie — a minor miscalculation, really — and that ARMs are perfectly safe as long as we use different acronyms and maybe require some income verification this time.

Never mind that the fundamental problem hasn't changed: housing prices remain completely detached from economic reality, wage growth continues its thirty-year nap, and interest rates are being manipulated by central banks trying to fight inflation they helped create through unprecedented money printing during the pandemic. But sure, let's solve the affordability crisis by offering people a mortgage that could reset to a payment they can't afford three years from now.

The Bigger Picture: A System Eating Itself

The resurgence of the ARM as a "solution" to housing affordability is a perfect microcosm of late-stage capitalism's autophagy. Rather than address the underlying disease — housing costs that have increased 4x faster than wages over the past two decades, private equity firms buying up single-family homes as investment vehicles, restrictive zoning that prevents new construction, and monetary policy that treats housing as a speculative asset class rather than a basic human need — we're offering buyers a slightly cheaper way to participate in their own eventual destruction.

It's the financial equivalent of treating a brain tumor with aspirin.

The ARM "discount" exists because lenders know something buyers apparently don't: interest rates, having risen dramatically, are unlikely to fall significantly in the near term. The Federal Reserve has made it clear that inflation remains stubbornly persistent, which means rates will stay elevated or possibly climb higher. Taking an ARM right now is betting that either rates will fall dramatically in the next few years (allowing you to refinance) or that you'll sell before the adjustment (assuming home prices continue rising).

Both assumptions require a level of optimism that borders on clinical delusion.

The Faustian Bargain

Every ARM is a Faustian bargain: present comfort in exchange for future risk. Sometimes that bet pays off. Sometimes you refinance successfully or sell at a profit. Sometimes the economy cooperates and rates fall.

And sometimes you end up featured in a 2027 news article about the foreclosure crisis, wondering how a $150 monthly savings led to financial ruin.

The truly perverse element is that the people most likely to choose ARMs are the people least able to absorb the risk — first-time buyers stretching to afford anything, families living paycheck to paycheck who see that $150 as the difference between qualifying and not qualifying, people who view homeownership as the last remaining path to building wealth in an economy that has systematically eliminated every other avenue.

These are not sophisticated real estate investors playing the rate spread for profit. These are ordinary people being offered a "discount" on a product that could destroy them.

The Oracle Speaks

Here is the truth the real estate industrial complex will not tell you:

If you need an ARM to afford the house, you cannot afford the house.

If saving $150 per month is the determining factor in your home purchase, you are one rate adjustment away from catastrophe.

If the only way to participate in homeownership is to accept significant future financial risk, the system is broken — not you.

The "biggest discount since 2022" is not a discount. It is a deferral. It is kicking the can down the road and hoping that road leads somewhere other than foreclosure court. It is the financial services industry, having learned absolutely nothing from 2008, selling the same poison in a different bottle to a new generation of desperate buyers.

And calling it a sale.

The Way Forward (Or: How We Got Here and Why We'll Do It Again)

The resurgence of ARMs is a symptom of a housing market so fundamentally diseased that buyers are willing to accept future risk for present access. It's a market where a $150 monthly payment difference is framed as savvy financial planning rather than evidence of systemic dysfunction.

We could fix this. We could build more housing. We could implement policies that treat homes as shelter rather than speculative assets. We could regulate the financialization of residential real estate. We could enforce lending standards that don't require exotic mortgage products to make homeownership accessible.

But that would require acknowledging that the current system is working exactly as designed — enriching financial institutions, real estate investment firms, and existing homeowners while pricing out new buyers and creating instability.

So instead, we'll celebrate the return of the ARM. We'll frame it as a "discount." We'll ignore the warnings tattooed across recent history. We'll pretend that this time is different, that we've learned our lessons, that the safeguards are sufficient.

And in five years, when the adjustments hit and the foreclosures begin, we'll act surprised.

Welcome to the American Dream, now available with adjustable rates and a side of amnesia. Your $150 monthly savings awaits. The bill comes later.

The Oracle Also Sees...

The $330,000 Bedroom-Free Dream: Long Island's Monument to Housing Market Dementia

For $329,900, Long Island offers you 446 square feet with no bedroom—proof that the housing market has finally achieved complete detachment from reality, sanity, and the English language.

The $330K Bedroom-Free Shoebox: American Real Estate's Final Descent Into Parody

A $329,900 Long Island tiny home with zero bedrooms has gone viral, perfectly encapsulating the housing market's descent into expensive, bedroom-free madness.

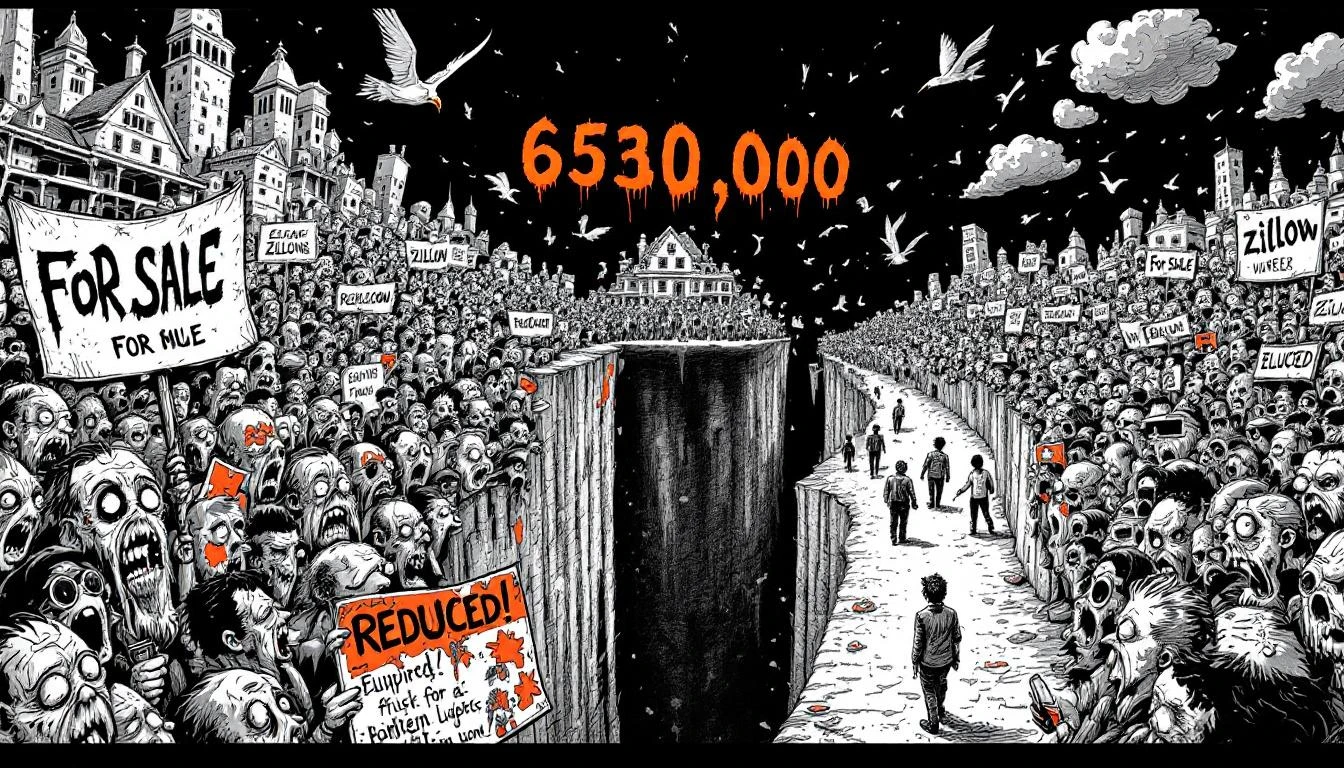

The Great Standoff: 630,000 Sellers Discover Nobody Wants Their Overpriced Shitboxes

630,000 more sellers than buyers—the largest gap on record. Turns out nobody wants to pay $800K for your 1987 tract home after all. The standoff begins.