The Great American Standoff: 630,000 Sellers Discover Nobody Wants Their Overpriced Shitboxes

The Emperor Has No Buyers

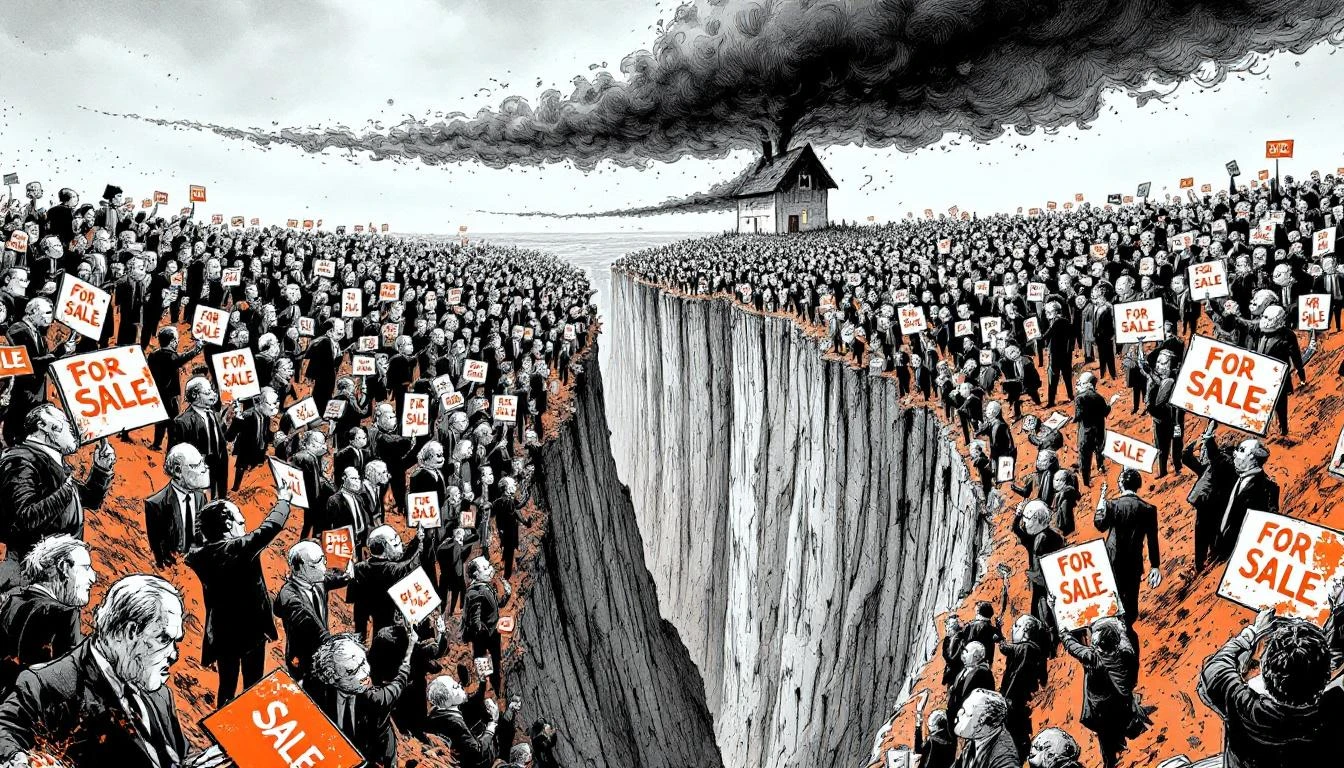

Behold, dear readers, the most glorious spectacle in American real estate since the last time we collectively lost our minds: 630,000 sellers standing in the marketplace like jilted lovers at a speed-dating event, clutching their listing agreements and wondering why nobody wants their "charming" 1,400-square-foot rancher for $847,000.

This is not merely a gap. This is a chasm. This is the Grand Canyon of delusion, measured not in geological time but in the precise moment when pandemic-era fever dreams collided with the cold, hard mathematics of affordability.

The Arithmetic of Absurdity

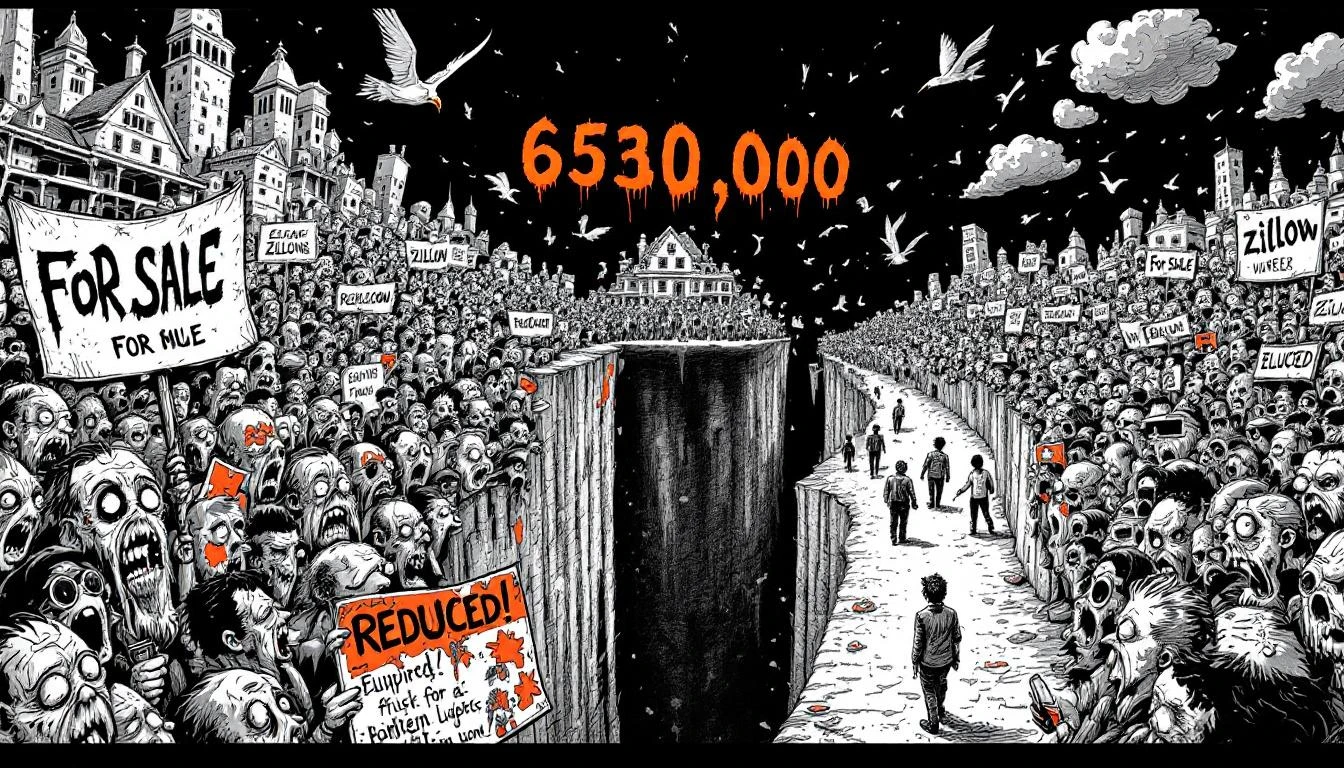

Let us parse the numbers, shall we? A 46.3% surplus of sellers over buyers. Nearly half again as many people trying to unload their properties as there are suckers—pardon me, valued customers—willing to take the bait. The largest gap since Redfin started tracking this data in 2013, which means we've officially entered uncharted waters in the annals of modern housing hubris.

This represents something far more profound than a market correction. This is the great reckoning, the moment when sellers who refinanced at 2.8% and watched their neighbors flip fixer-uppers for six-figure profits suddenly discovered that musical chairs has ended, the music has stopped, and they're the ones left standing with a mortgage they can't afford and a listing that's been sitting on Zillow longer than milk in a desert sun.

The Lock-In Effect, or: How I Learned to Stop Worrying and Love My Underwater Asset

The so-called "lock-in effect"—that delightful phenomenon where homeowners with sub-3% mortgages refuse to sell because they'd have to buy back into the market at 7%—has created a perverse prisoner's dilemma. Everyone wants out, but nobody wants to admit they're trapped. So they list at fantasy prices, prices that assume the buyer pool consists entirely of cryptocurrency billionaires and trust-fund babies fleeing their coastal enclaves.

Spoiler alert: It doesn't.

The typical American worker, crushed between stagnant wages and explosive living costs, cannot afford your "cozy" three-bedroom with "potential" (translation: needs $80,000 in immediate repairs) at $650,000. They cannot afford it at $550,000. They probably can't afford it at $450,000, but you'll never drop the price that low because you "know what you have" and "somebody will pay it eventually."

Eventually is a long time to carry two mortgages, friend.

The Mythology of Perpetual Appreciation

Somewhere along the way, we convinced ourselves that home prices only go up. That real estate is a perpetual motion machine of wealth generation, immune to the laws of economic gravity that govern everything else. We forgot 2008, or perhaps we simply decided it was an aberration, a glitch in the Matrix that couldn't possibly repeat itself because this time is different.

This time is not different. This time is the same story wearing different clothes: a speculative mania followed by a reality check, written in the universal language of overextended credit and magical thinking.

The 630,000-seller surplus isn't an anomaly. It's a symptom. A symptom of a housing market that's been disconnected from income fundamentals for so long that we forgot houses are supposed to be homes first and investments second. We've spent two decades treating shelter—the most basic human need after food and water—as a casino chip, and now we're shocked, shocked to discover that the table has limits.

The Buyer's Revenge

For the first time in over a decade, buyers have leverage. Real, actual, negotiating power. They can lowball. They can demand concessions. They can walk away from inspections that reveal foundation cracks and knob-and-tube wiring without feeling like they've just passed up their only chance at homeownership before prices spiral further into the stratosphere.

This terrifies sellers, who've grown accustomed to bidding wars and waived contingencies and offers $50,000 over asking, cash, sight unseen. They've forgotten what it's like to actually compete for a sale rather than simply listing and watching the offers roll in like tide at Omaha Beach.

Welcome to the free market, ladies and gentlemen. It cuts both ways.

The Prophetic Conclusion

So here we stand, at the precipice of what might charitably be called a "correction" and what honest observers recognize as the beginning of a long, painful deflation of the most absurd asset bubble in modern American history. Six hundred thirty thousand sellers are about to learn a very expensive lesson about the difference between list price and sale price, between what you think your house is worth and what someone will actually pay for it.

The smart ones will drop their prices now, take their losses, and move on. The delusional ones will hold out for "the right buyer," watching their carrying costs accumulate like interest on a payday loan while the market continues its inexorable march toward rationality.

Place your bets accordingly. The house always wins, except when it's your house, and nobody wants to buy it.

The Oracle has spoken. The market will correct. Gravity remains undefeated.

The Oracle Also Sees...

The $330,000 Bedroom-Free Dream: Long Island's Monument to Housing Market Dementia

For $329,900, Long Island offers you 446 square feet with no bedroom—proof that the housing market has finally achieved complete detachment from reality, sanity, and the English language.

The $330K Bedroom-Free Shoebox: American Real Estate's Final Descent Into Parody

A $329,900 Long Island tiny home with zero bedrooms has gone viral, perfectly encapsulating the housing market's descent into expensive, bedroom-free madness.

The Great Standoff: 630,000 Sellers Discover Nobody Wants Their Overpriced Shitboxes

630,000 more sellers than buyers—the largest gap on record. Turns out nobody wants to pay $800K for your 1987 tract home after all. The standoff begins.