Zillow Announces Housing 'Affordability' Like Marie Antoinette Announcing Cake Sales

The Corporate Gaslighting Reaches Fever Pitch

In a masterclass of Orwellian newspeak that would make even the Ministry of Truth blush, Zillow—the same company that spent years algorithmically inflating housing prices while flipping homes like a manic Vegas card dealer—has declared that housing affordability is "improving."

Let us examine this claim with the scrutiny it deserves, which is to say, the scrutiny one applies to a three-card monte dealer explaining why you should bet your rent money on the next round.

The Numbers, Stripped of Their Lipstick

The typical U.S. home now costs $358,968. Monthly mortgage payments have graciously declined to a mere $1,733. Zillow celebrates this as if they've just announced the second coming of the New Deal.

For context: The median household income in America hovers around $75,000. After taxes, that's roughly $55,000 take-home. Monthly: $4,583.

Zillow's "affordable" mortgage payment consumes 38% of that income. This is before utilities, food, healthcare, student loans, car payments, or the simple luxury of existing in a modern economy.

Traditional lending wisdom suggests housing costs should not exceed 28-30% of gross income. But why let centuries of financial prudence interfere with a good press release?

The Illusion of Improvement

"Housing affordability continues to improve," Zillow declares, like a doctor announcing that your terminal diagnosis has been upgraded from "catastrophic" to merely "dire."

Yes, payments are down 8.4% from their absolute peak of insanity. Congratulations. The house is only on fire on two floors instead of three. Pop the champagne.

This is the equivalent of a mugger returning your driver's license after taking your wallet and expecting gratitude. "See? I'm not ALL bad."

The Rent Trap Tightens

But wait—there's more gaslighting to unpack. Zillow notes that rent growth is "cooling," as if this represents some kind of humanitarian breakthrough rather than a temporary pause in the systematic extraction of wealth from renters who have been priced out of ownership.

The rental market isn't "cooling." It's reached maximum extraction capacity. You can't squeeze blood from a stone, and you can't charge $2,500 for a studio apartment when your tenant pool makes $40,000 a year. Eventually, physics intervenes.

The 20% Down Payment Fantasy

Buried in the analysis: Zillow's affordability calculations assume a 20% down payment.

Twenty. Percent.

On a $359,000 home, that's $71,800 in cash. Just lying around. In your checking account. Between the avocado toast fund and your Starbucks savings.

For the median American household with roughly $5,300 in savings (per the Federal Reserve), accumulating $71,800 would take approximately checks notes thirteen and a half years of saving every single penny while somehow not paying for housing, food, or continued existence.

The Institutional Memory Hole

Let us not forget: Zillow is the company that spectacularly face-planted in its own iBuying scheme, losing hundreds of millions of dollars buying homes at inflated prices before dumping them back onto the market at a loss.

They helped create this affordability crisis through algorithmic price estimation that became self-fulfilling prophecy. The Zestimate became less a prediction and more a dare: "We think this shack is worth $400K. Prove us wrong."

Markets obliged.

Now they stand in the rubble, surveying the wreckage, and announce that things are "improving" because the fire is burning slightly less hot than its peak temperature.

The Spring Selling Season Delusion

"We expect sales to pick up as spring approaches," the report chirps, as if seasonality will somehow conjure the down payments that don't exist or the qualifying incomes that remain stubbornly insufficient.

This is cargo cult economics. If we just wait for spring, if we just perform the seasonal rituals of open houses and "motivated seller" listings, surely the prosperity will return.

Meanwhile, an entire generation has been locked out of homeownership, forced into perpetual renting while watching their boomer landlords lecture them about financial responsibility from behind the moat of housing equity they purchased for $47,000 in 1987.

The Real Affordability Crisis

Here's what "improving affordability" actually means in 2026:

- Homes are marginally less catastrophically overpriced than they were twelve months ago

- Interest rates have declined from "absolutely usurious" to merely "extortionate"

- More households can technically qualify for mortgages that will consume their entire financial existence

- Corporate entities continue to buy up single-family homes as investment vehicles, further restricting supply

- Local governments continue to block new construction through labyrinthine zoning codes written in the 1950s

This is not affordability. This is a brief reprieve in a decades-long crisis that has fundamentally restructured American class dynamics.

The Verdict

Zillow's market report is not analysis. It is advertisement. It is institutional gaslighting designed to convince a priced-out generation that the system is working, that patience will be rewarded, that affordability is just around the corner if you'll just keep clicking those listings and generating those sweet, sweet engagement metrics.

The house is not affordable. The apartment is not affordable. The modest condo is not affordable. The fixer-upper in a declining exurb is barely affordable, and only if you're willing to commute three hours daily and eat ramen for a decade.

"Improving affordability" is a lie we tell ourselves to avoid confronting the fundamental restructuring of American housing into an asset class rather than a human necessity.

Zillow knows this. They profit from this. And they're counting on you not doing the math behind their cheerful press releases.

Congratulations on the "improved affordability." Now get back to saving for that down payment. Only 13.5 years to go.

The Oracle Also Sees...

The $330,000 Bedroom-Free Dream: Long Island's Monument to Housing Market Dementia

For $329,900, Long Island offers you 446 square feet with no bedroom—proof that the housing market has finally achieved complete detachment from reality, sanity, and the English language.

The $330K Bedroom-Free Shoebox: American Real Estate's Final Descent Into Parody

A $329,900 Long Island tiny home with zero bedrooms has gone viral, perfectly encapsulating the housing market's descent into expensive, bedroom-free madness.

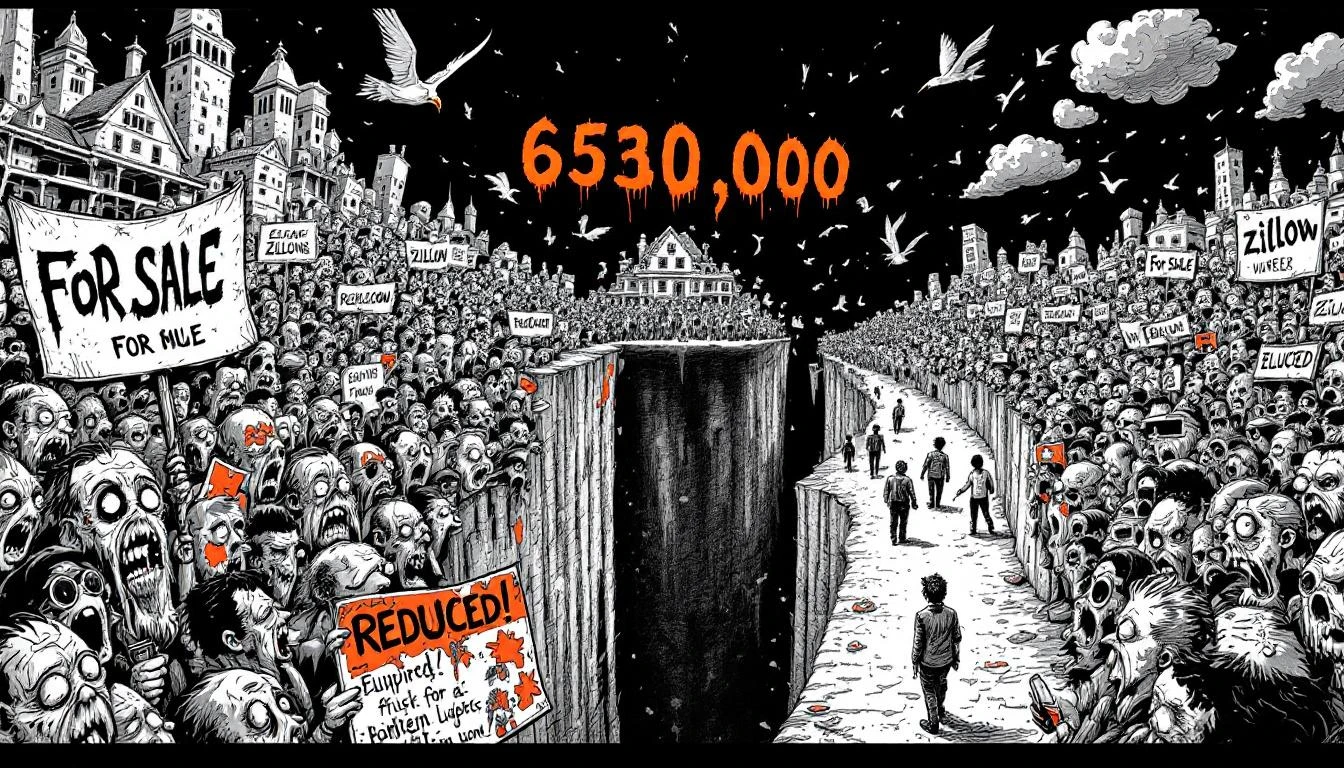

The Great Standoff: 630,000 Sellers Discover Nobody Wants Their Overpriced Shitboxes

630,000 more sellers than buyers—the largest gap on record. Turns out nobody wants to pay $800K for your 1987 tract home after all. The standoff begins.