Zillow Declares Victory Over Affordability Crisis It Helped Create

The Arsonist Returns to Admire the Ashes

There's a particular species of corporate audacity that only blooms in the fetid soil of American real estate: the kind where the company that spectacularly immolated $881 million in a house-flipping scheme—driving up prices in dozens of markets while algorithmic greed ran wild—now stands before us, clipboard in hand, to declare that housing is "improving in affordability."

Zillow's January Market Report arrived this week like a hostage video from economic reality. The headline? Affordability is improving! The fine print? The "typical" American home now costs $358,968, and your monthly mortgage payment has graciously declined to a mere $1,733. That's down 8.4% from last year, they crow, as if we should prostrate ourselves in gratitude.

Let's decode this Orwellian mathematics: When your monthly payment drops because the asset price remains catastrophically inflated but the interest rate needle moved slightly—that's not affordability. That's a different configuration of the same financial waterboarding.

A Brief History of Zillow's Philanthropic Endeavors

Cast your mind back to 2021, when Zillow Offers was buying houses like a cocaine-addled Monopoly player, using predictive algorithms that somehow managed to predict everything except that buying high and selling low is bad business. They purchased 27,000 homes, helped inflate prices in competitive markets, then dumped the inventory at a loss when their AI oracle discovered what medieval peasants already knew: you can't eat algorithms.

The company laid off 2,000 employees. Rich Barton, CEO, kept his job. The housing market kept the scars.

Now here's Zillow—not a government agency, not a housing advocacy nonprofit, but a real estate listing platform whose revenue model depends on transaction volume—telling us it's a great time to buy.

The Gaslighting Symposium

"Housing affordability continues to improve for prospective homebuyers," intones Skylar Olsen, Zillow's chief economist, as if she's describing weather patterns rather than the systematic hollowing-out of the American middle class's ability to build wealth through homeownership.

Let's examine this "improvement":

- The median home price remains roughly double what it was in 2012

- Real wages have barely kept pace with general inflation, let alone housing inflation

- A $359,000 home requires roughly $72,000 down payment for a conventional mortgage

- That monthly payment of $1,733? It's 43% higher than it was in January 2020

But sure, because it's 8.4% cheaper than the absolutely unhinged peak of last year, we're supposed to throw a parade.

Spring Loading the Trap

"We expect sales to pick up as spring approaches," the report cheerfully predicts. Translation: Please, for the love of our quarterly earnings, somebody buy something.

Zillow doesn't make money when you rent. They don't profit when you stay put. They certainly don't benefit when you organize tenants' unions or demand policy changes. They make money when you transact—when you list, when you buy, when you click, when you dream of homeownership while scrolling through properties you'll never afford.

This is economic horoscope writing disguised as market analysis. "The stars are aligning for buyers!" (Jupiter is in the fifth house of commission revenue.)

The Ministry of Truth's Shelter Inflation

My favorite bit of linguistic gymnastics: "modest growth in the Zillow Observed Rent Index points to continued cooling in shelter inflation."

Modest growth. Cooling inflation.

Rents are still increasing—just at a slightly slower rate of increase. This is like saying the floodwaters are "improving" because they're only rising two inches per hour instead of three. You're still drowning, but statistically, you're drowning better.

The Zillow Observed Rent Index isn't some neutral scientific instrument. It's a proprietary metric from a company with billions of dollars in interests aligned with maintaining high housing costs. Asking Zillow about housing affordability is like asking Philip Morris about lung health trends.

The Theology of Market Timing

Here's what Zillow won't tell you in their monthly market hosannas:

They have no idea what happens next. Nobody does. They couldn't predict their own house-flipping apocalypse when they were literally the ones doing it.

"Affordability" is relative to complete disaster. Yes, it's more affordable than the peak of a speculative bubble. So is everything when you time it right.

They need you to believe it's always a good time to buy. Their business model is heroin dealer logic: the first hit is information, but you only get hooked when you transact.

The Oracle's Decree

When the company that turned housing into an algorithmic casino—that bought houses as speculative assets, that helped normalize the financialization of shelter, that literally had to shut down its entire home-buying division because its models were catastrophically wrong—when that company tells you affordability is improving?

Remember this: Zillow isn't your friend. They're not a public service. They're not even particularly good at their own business model. They're a traffic monetization engine wrapped in aspirational real estate porn, and every "market report" is an advertisement for their own relevance.

Housing affordability isn't "improving" in any meaningful sense. It's just less historically catastrophic than it was twelve months ago. The difference between burning alive and burning slightly slower is not comfort—it's torture with better PR.

The American Dream isn't on sale. It's just been repriced from "impossible" to "nearly impossible," and the company selling you the listing wants you to know: What a bargain!

Epilogue: A Modest Proposal

Perhaps we should thank Zillow for their service. After all, without their monthly market reports, how would we know that the unaffordable is becoming slightly less unaffordable? How would we understand that our financial strangulation is easing from a chokehold to merely a firm grip on the throat?

In the future, maybe Zillow could expand their benevolent market analysis to other sectors. "Insulin prices improve as cost drops from catastrophic to merely ruinous." "Childcare affordability surges as average family only needs 1.8 full-time jobs to cover costs."

Until then, we'll file this report where it belongs: in the same folder as "Tobacco Industry Finds Smoking Rates Encouraging" and "Oil Companies Declare Climate Concerns Overblown."

The gaslighting will continue until morale improves.

—The Oracle

The Oracle Also Sees...

The $330,000 Bedroom-Free Dream: Long Island's Monument to Housing Market Dementia

For $329,900, Long Island offers you 446 square feet with no bedroom—proof that the housing market has finally achieved complete detachment from reality, sanity, and the English language.

The $330K Bedroom-Free Shoebox: American Real Estate's Final Descent Into Parody

A $329,900 Long Island tiny home with zero bedrooms has gone viral, perfectly encapsulating the housing market's descent into expensive, bedroom-free madness.

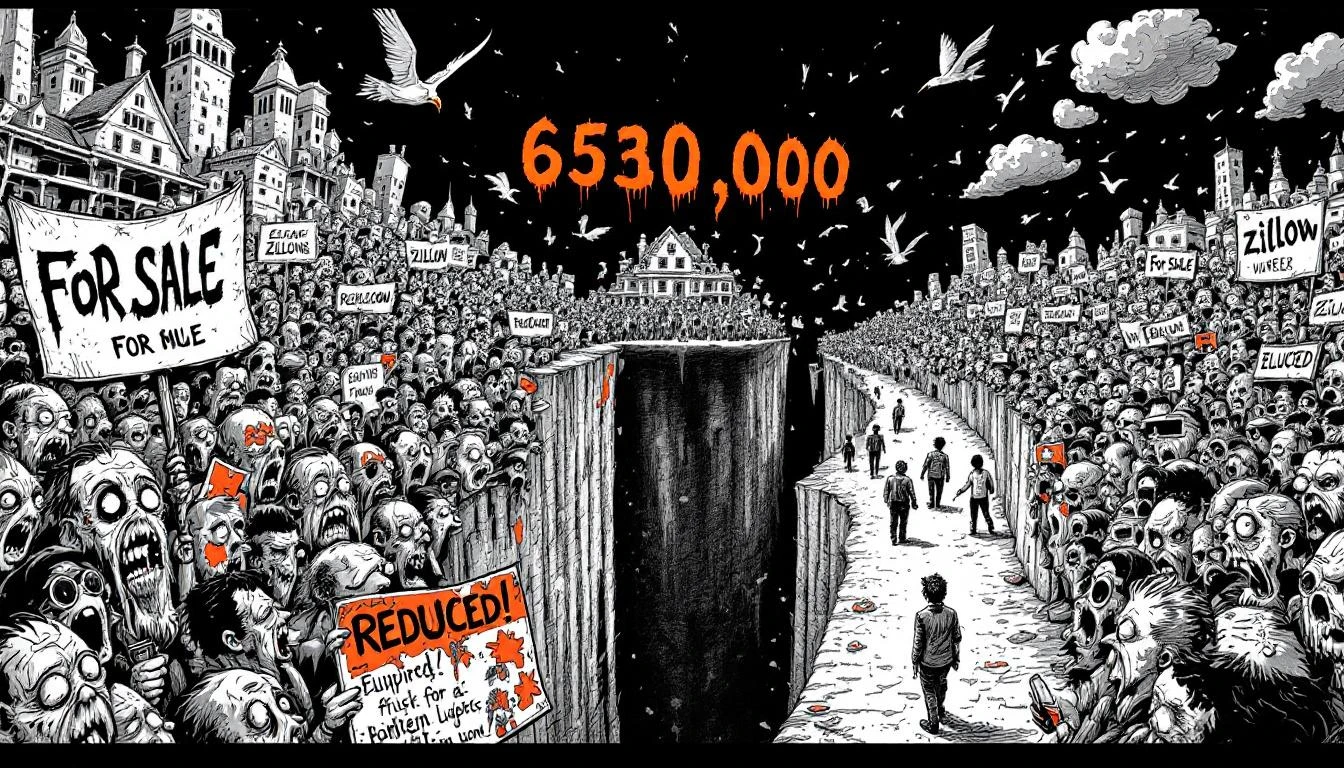

The Great Standoff: 630,000 Sellers Discover Nobody Wants Their Overpriced Shitboxes

630,000 more sellers than buyers—the largest gap on record. Turns out nobody wants to pay $800K for your 1987 tract home after all. The standoff begins.