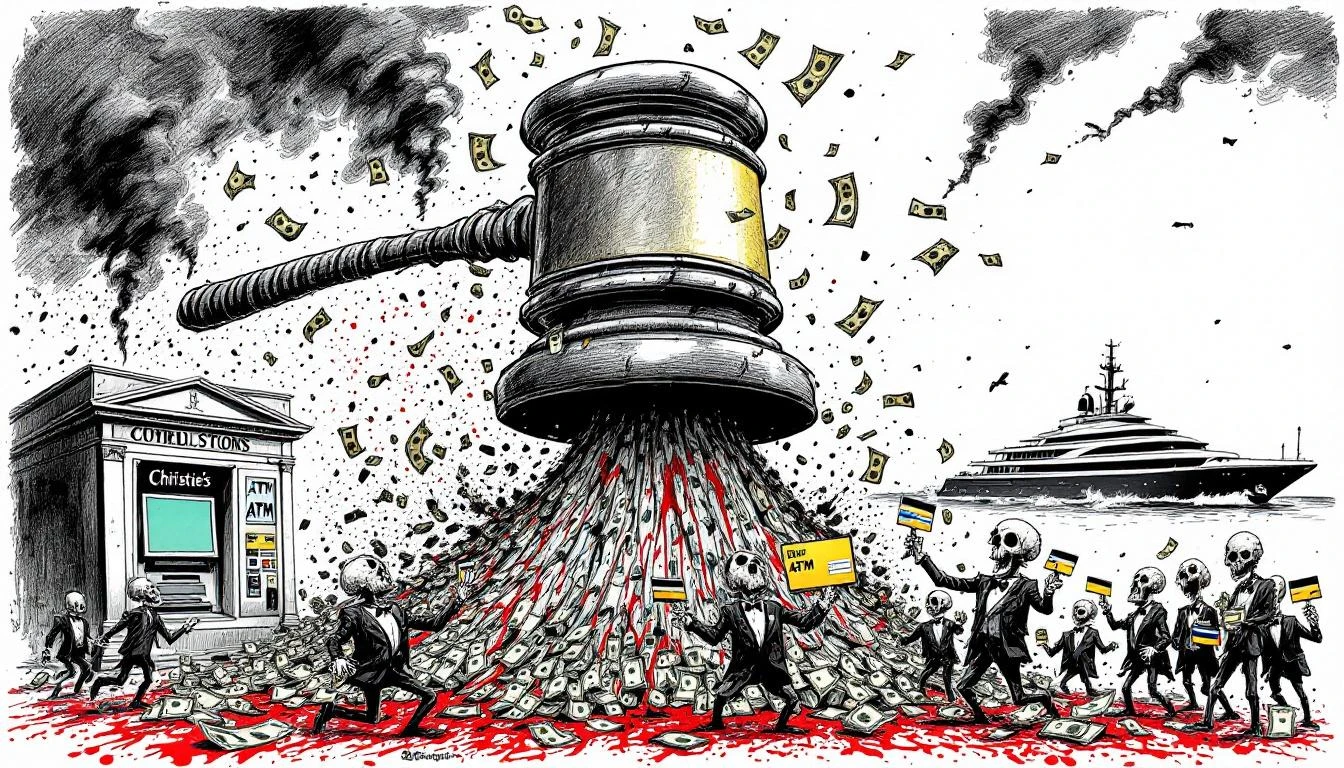

Twelve Records in One Night: The Sotheby's Method of Manufacturing Legitimacy

The Miracle of Multiplication

When Sotheby's announced it had set twelve—count them, TWELVE—auction records for South Asian artists in a single evening, the art world was expected to genuflect before this statistical miracle. Never mind that breaking a dozen records simultaneously is less a sign of organic market enthusiasm than a flashing neon sign reading "WE CONTROL THE ENTIRE VALUATION APPARATUS."

The $22.1 million sale was hailed as proof of "surging demand" for South Asian art. What it actually proved is that when you're the house that quite literally invented the market category in 1995, you can engineer scarcity, manufacture benchmarks, and crown yourself kingmaker while collecting a nice percentage on both ends.

The Alchemy of Artificial Scarcity

Here's how the magic trick works: First, ignore an entire region's artistic output for most of your 279-year history. Then, in the mid-1990s, "discover" it with the missionary zeal of a colonizer planting a flag. Establish yourself as the sole arbiter of value by holding the only major auctions. Set initial records so low that a regional artist selling for $30,000 counts as a "breakthrough." Wait patiently.

Then—and this is the beautiful part—you slowly ratchet up estimates, whisper to collectors about "emerging markets," and watch as each subsequent sale sets a "record" that you yourself established six months prior. It's not market manipulation if you call it "market making."

The fact that these records were broken by margins like $300—literally raising an artist's lifetime achievement high-water mark by the cost of a decent dinner—reveals the game. When Mohan Sharma's "record" eclipsed his previous "record" (also set at Sotheby's, naturally) by a mere $345, we're not witnessing the invisible hand of the market. We're watching a house play both dealer and appraiser in a casino where they also print the chips.

The Gatekeepers Declare Themselves Liberators

Sotheby's press materials trumpet their role in "cementing South Asian art as one of the most dynamic fields in global collecting." Translation: We ignored your artists until we figured out how to monetize them, then graciously allowed them into our velvet-roped sanctum—for a 25% commission, naturally.

The language is always the same: "establishing the market," "setting benchmarks," "achieving record-breaking results." What they never say is that they're not documenting value—they're inventing it. They're not responding to demand—they're creating it through the theatrical presentation of scarcity and the self-referential citation of their own previous sales.

Consider: When every lot sells (100% sell-through rate, they crow), you're either witnessing unprecedented unanimous desire or rigged reserve prices. When 95% of works sell above estimate, you're either seeing market euphoria or deliberately sandbagged estimates designed to generate headline-friendly "exceeded expectations" coverage.

The Colonial Economics of Cultural Validation

There's a particular postcolonial irony in watching a British-founded auction house position itself as the validator of South Asian artistic achievement. For decades, these artists created, exhibited, and traded their work in thriving regional markets. They had value. They had audiences. They had legitimacy.

But that legitimacy didn't count—not in the ledgers that matter to the global collecting class—until Sotheby's declared it so. Until Western institutional blessing was conferred. Until the prices were translated into dollars and euros and the artists' names were printed in catalogs designed to look like museum publications.

The message is clear: Your art isn't really worth anything until we say it is. Your records aren't real until we set them. Your market doesn't exist until we establish it. It's the same civilizing mission in different clothes—but now instead of stealing artifacts for museums, they're extracting percentages while positioning themselves as benevolent discoverers.

The Mathematics of Manufactured Hype

Let's talk numbers. When S.H. Raza's painting sold for $5.6 million on an estimate of $2-3 million, Sotheby's called it "smashing the artist's previous record." What they didn't emphasize is that they set that previous record too—just last March, for $1.33 million. In one year, they quadrupled their own benchmark.

Either Raza suddenly became four times more important to art history, or someone realized they'd been leaving money on the table. The sudden discovery that a dead artist's work is worth 400% more than previously thought doesn't suggest market maturation—it suggests the previous valuations were purely arbitrary.

Breaking twelve records in one night isn't a sign of a healthy, organic market. It's a sign of a rigged game where the house controls the baseline, the increment, and the press release.

The Endgame

What happens when the regional collectors who actually care about these artists can no longer afford them? When Vivan Sundaram and Vasudeo Gaitonde become investment vehicles for wealth parking rather than cultural touchstones? When the artists' own communities are priced out of their heritage?

Sotheby's doesn't care. They've already moved on to the next "emerging market" to "establish." The auction house business model requires fresh territory—new regions to discover, new categories to invent, new records to break. Southeast Asian art. African contemporary. Indo-Pacific photography. The formula is infinitely replicable.

They're not building markets. They're building monuments to their own gatekeeping power, brick by brick, record by manufactured record.

The Prophet's Verdict

When an institution can break twelve records in one night, it's not documenting value—it's dictating it. When a single sale "underscores surging demand," it's not responding to the market—it's manufacturing the narrative of the market.

Sotheby's hasn't made South Asian art valuable. South Asian art was always valuable—to the people who created it, collected it, and lived with it long before the auction houses arrived with their gavels and their catalogs and their self-congratulatory press releases.

What Sotheby's has done is insert itself as the mandatory middleman between artists and legitimacy, between value and validation, between cultural production and global recognition. They've built a tollbooth on the road to institutional acceptance and called it market making.

Twelve records in one night. Twelve opportunities to collect commissions. Twelve headlines to generate future consignments. Twelve data points in a self-referential system that exists primarily to justify its own existence.

It's not a market. It's a protection racket dressed up as cultural stewardship.

And the house always wins.

The Oracle Also Sees...

The Ballpoint Barons and the Case of the Chauffeur Who Allegedly Knew Fra Angelico

Heirs to the Bic pen fortune are battling a Chilean billionaire over a Fra Angelico they didn't notice was missing for twelve years. The chauffeur did it, apparently. Or did he?

The Biennale of Short Memories: How Venice Learned to Stop Worrying and Love the Pavilion

Russia returns to Venice after four years, proving institutional memory lasts exactly as long as one exhibition cycle. Outrage has a shelf life; prestige is eternal.

The Newhouse Estate: How Christie's Turns Inherited Taste Into Half a Billion Dollars of Nostalgia for When Art Meant Something

Christie's preps another $450M bite of the Newhouse estate—led by a $100M Pollock—proving once again that inherited taste is just another asset class for the auction house oligopoly to liquidate.